01

Forty-four markets, one grid

Equities, FX majors, precious and industrial metals, energy, rates — every underlying that matters to a derivatives book, in one screen, one schema, one set of percentiles.

CrossVol Research publishes non-consensus thesis notes on macro volatility, derivatives positioning, and cross-asset transmission. Each note starts from a single observation the sell-side is mispricing, and ends where the trade actually lives.

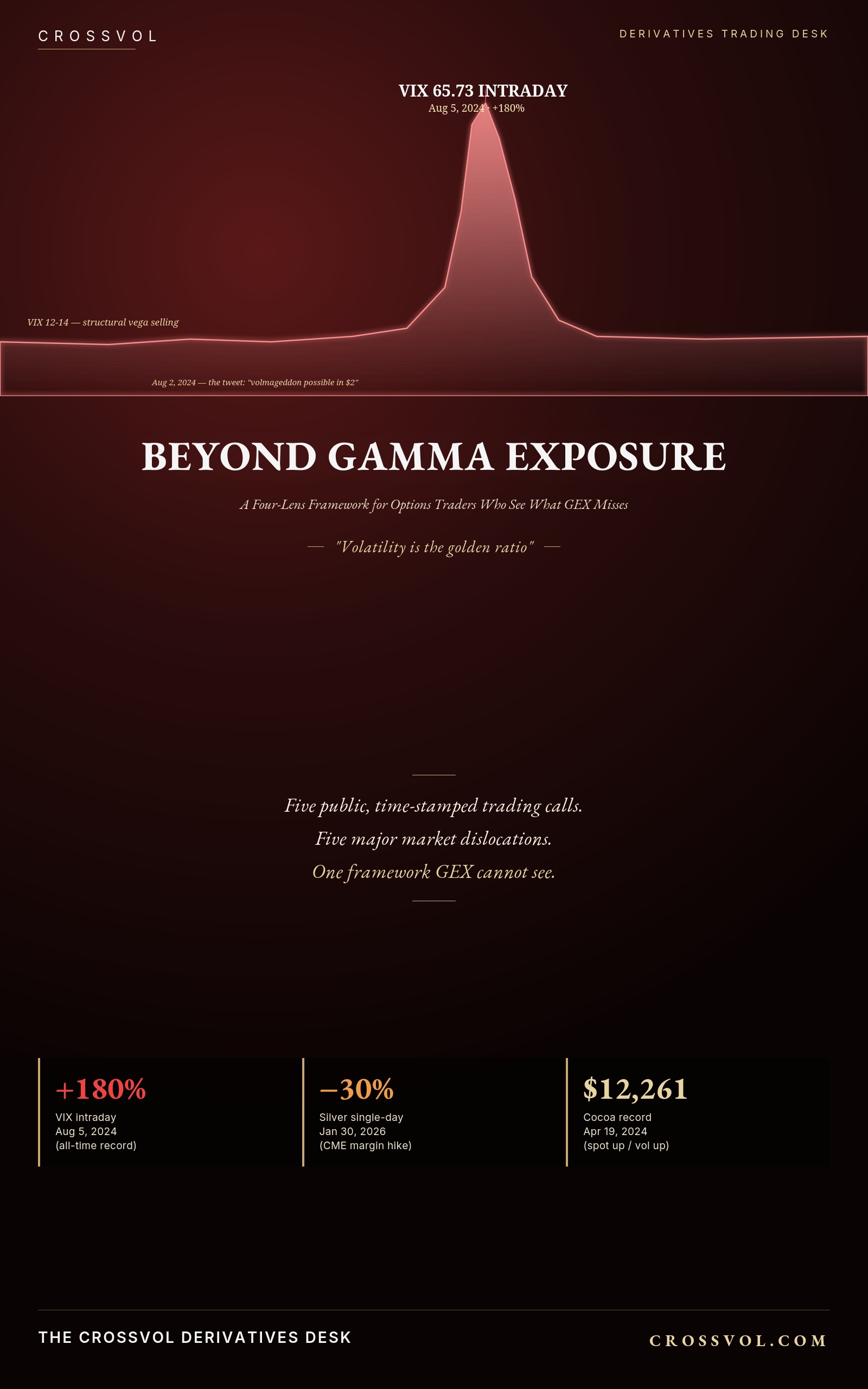

The world over-reads gamma. It under-reads everything else. Every major dislocation since August 2024 — the volmageddon, the DeepSeek crash, the Trump tariffs sell-off, the silver squeeze — was forecast not by Gamma alone, but by the lens that everyone else had stopped watching. CrossVol exists to make that lens permanent, routine, and within reach.

The capabilities a derivatives desk actually needs in production. Not a feature checklist — a daily routine that ships.

Equities, FX majors, precious and industrial metals, energy, rates — every underlying that matters to a derivatives book, in one screen, one schema, one set of percentiles.

Every metric is back-tested against five years of historical data. No raw value without its 1-day, 1-month, 1-year percentile. Every reading anchored in regime context.

CrossVol watches the four lenses simultaneously. When three out of four cross threshold in the same session — the alert lands before the move materializes on the chart.

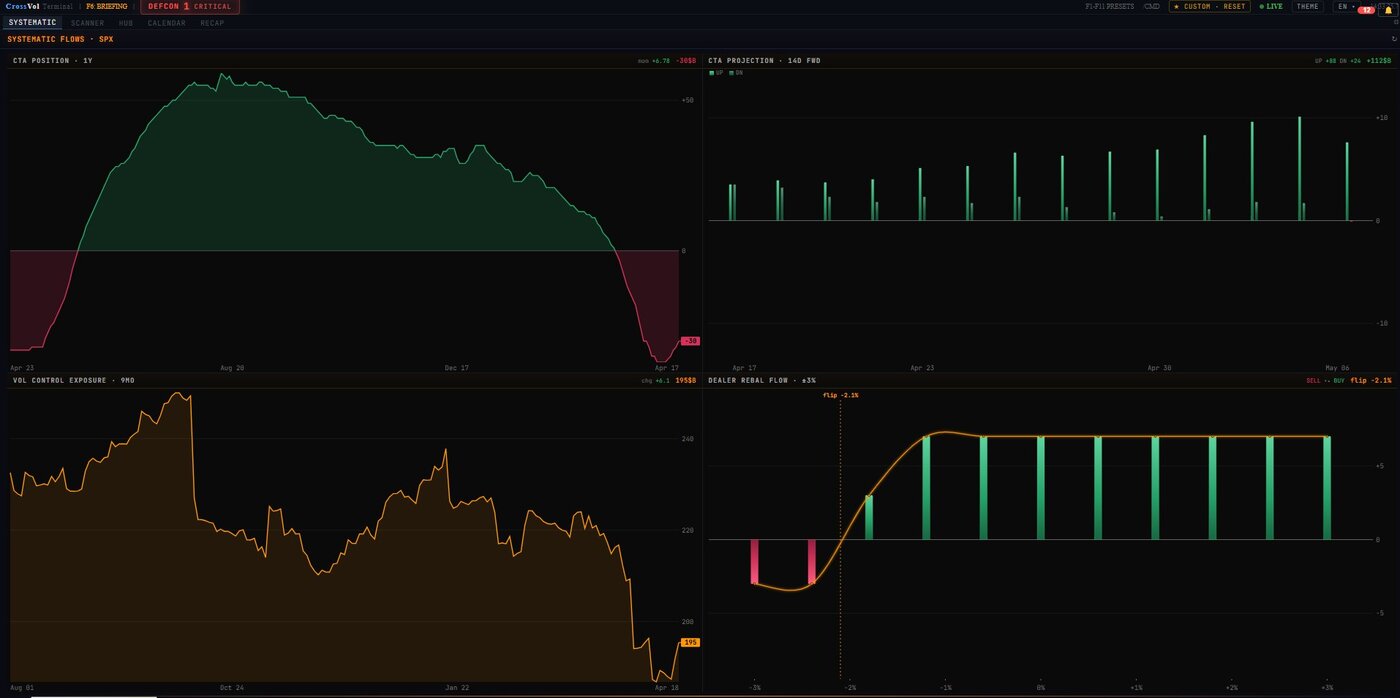

Lease rates, LME and COMEX inventories, calendar spreads, contango regimes. The non-options layer that anticipates commodity dislocations weeks ahead.

Every morning, the framework applied to the current regime. Not a generic newsletter. The same routine the desk runs internally — published, dated, signed.

No survivorship bias. Every call from the desk is posted on X before the move, time-stamped, never edited. The track record is auditable, by anyone, at any time.

Where dealers stand. Where the spot magnetism comes from.

Listed-options aggregation. Flip-zones, walls, charm decay. The lens most retail watches — and the one that misses OTC structured flows.

Who is short volatility. Where an unwind begins.

Income funds, autocalls, ETP flows aggregated into a single read. VVIX/VIX divergence as early-warning bell. Three of five dislocations since August 2024 started here.

What the market pays for upside versus downside.

The fear-greed gauge that price action lags by days. 25-delta skew across equities, FX, commodities — the cross-asset language of regime change.

How stress distributes across time.

VIX curve, lease rates, calendar spreads, physical inventories. The slowest-moving lens. Also the most reliable warning when it stops moving.

Each view exists because a real trade — one we publicly dated — needed it. No widgets for the sake of widgets.

Dealer Vega aggregated across listed options, variance swaps, structured products and ETP flows. When VVIX/VIX breaches its 30-day mean by two standard deviations, you have a two- to three-week window to position before compression releases.

LBMA lease rates, LME inventories, calendar spreads, listed-options Risk Reversal — four inputs, one composite score. On 2 February 2026, three days before silver lost 30%, the score sat at 87 of 100.

USD/JPY 25-delta RR, VIX term-structure slope, MOVE Index lined up in a single grid. When all three flip in the same session, the framework signals a 73% directional probability over the last two-year backtest.

CrossVol does not replace your platform. It threads a coherent reading across the day — from Asia open to US close — and hands you a single grid at each transition.

Overnight Asia session digested. VVIX/VIX divergence, MOVE Index move, FX RR shifts. The brief lands in your inbox.

SX5E autocalls position, Bund vs US10Y RR, copper LME inventory print. Bridge from EU to US session.

SPX gamma flip-zone, NDX dealer positioning, VIX term-structure slope. The four-lens read at the moment volume floods.

Day P&L, threshold-breach log, watchlist for next session. Confluence score updated for every covered underlying.

Three hundred and twenty pages. Nine chapters. Five dated war stories disassembled and rebuilt through the four lenses — the 5 August 2024 VIX spike, the 27 January 2025 DeepSeek crash, the 8 April 2025 Trump tariffs sell-off, the 5 February 2026 silver squeeze, the 2025 dispersion call.

Written for desk professionals who need a coherent language across asset classes, and for serious independent traders ready to stop reading the single lens everyone else watches.

Now live on Amazon — English edition. Additional languages rolling out (ES · DE · IT · NL · PL · SV · PT · AR · JA · ZH · HI · KO · RU · ID · VI).

The book lives free in its sample form. The terminal pays for the data, the percentiles, the daily routine.

Read the framework. Watch the public calls.

The four lenses on the underlyings that matter.

Live data, API, team integration.

No advertising. No dark patterns. No data resale. Cancel any time — one click.

One regime read per day. Written by the desk, applied to the four lenses, delivered before the European open. Free for the first thirty days — no credit card.

Used by traders at multi-strategy hedge funds, prop desks, and family offices. Unsubscribe in one click.

"When the spot-vol correlation flips, don't argue. Close your positions. Watch. Learn."

Lausanne · 6 September 2011 · The lesson that built the framework